|

property investment is not going to do better than a share portfolio, is all the hassle associated with property investment really worth it?

If you want to invest successfully in property, you have to follow certain rules:

- You must use debt finance – you have to take on a mortgage bond – to get a gearing effect.

- You have to hold property for a long time – at least 10

years, often much longer – to get a return that matches shares. This is partly because the transaction costs on property are so high (ie, you need a 10% increase in house prices just to cover your entry and exit costs), and partly because it takes time to reduce debt to a point where it is working in your favour.

- You must keep the rental income flowing. If your property stands without a tenant for one or two months a year, on average, it has a surprisingly negative effect on your overall return.

- You have to find a property that can give a reasonable gross rental yield – at least 8% per annum in the current market – otherwise the negative cash flow creates a debt burden. Finding properties that command a high enough rental is often easier said than done.

The Pros and Cons of Property and Shares

As we said above, owning your own home is almost always a good idea – assuming you're going to be in the same place for a reasonable length of time – because the rent you would pay elsewhere can go towards your bond repayments. But if you're looking at a second property as an investment, there are a number of things to consider. Given the fact that your property investment is unlikely to do better than a stock portfolio over time, the real question is whether you want to deal with the various complications of property ownership.

Here is a list of things to consider:

- As we said, property bought for cash is generally not a great investment. Are you able to get a mortgage bond? Are you happy to shoulder the debt? Bear in mind that if you are unlucky and the property market goes against you, you will still owe the money to the bank. This is the unfortunate position that property investors in America and England found themselves in after the crash of 2008 – property prices fell, many people owed more than there homes were worth, and some couldn't afford the bond repayments.

- Dealing with tenants and maintenance issues can be time-consuming and you need to allow for this. By contrast, your share portfolio will never phone you in the middle of the night to report a burst geyser.

- The costs associated with property ownership should not be underestimated. The property needs to be insured. Rates and taxes are typically paid by the owner, not the tenant. Maintenance is for the account of the owner – and properties do require maintenance. All of these costs have to be paid before rental income can be applied to bond repayments.

- Collecting rent is not always hassle-free. Non-payment and difficulty of ejecting bad tenants is a major problem with property investment, especially (although not exclusively) at the lower end of the market. Collection agencies are a good idea (many real estate companies provide this service), but this will reduce your rental yield by 8% to 10% per annum. Dividends from shares, on the other hands, require no special effort to collect. As a rule, after-tax dividends from value shares are not dissimilar to the net rental yield (after tax and all costs) from property.

- Property is illiquid – it's hard to convert property into cash if you need it in a hurry. It can easily take six months from deciding to sell to actually getting your money. Shares, on the other hand, can be converted into cash almost instantly.

- The transaction costs on property are very high. In addition to a deposit, you also need between 6% and 8% of the property value available to meet transfer duties, legal costs and other acquisition fees. Shares, on the other hand, can be acquired at well under 1% of capital value.

- Property is definitely less volatile than the share market, and this can be an advantage. With both shares and property, however, you never want to be in a position where you are a forced seller. If you do have to sell, you want to be able to sell into a strong market. This means taking a long-term view and not over-exposing yourself. The ever-present danger with property investments is that the debt you take on becomes a problem.

Risks

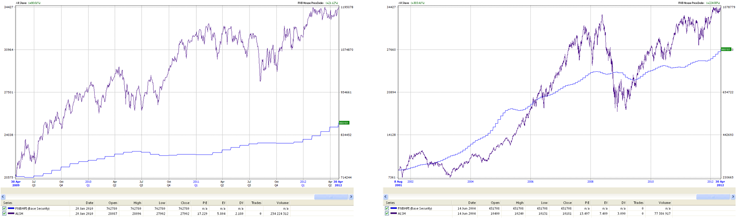

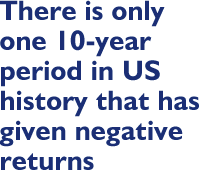

But the stock market is dangerous, we hear some people say. There is certainly a widespread perception that shares are riskier than property, and this is not without some basis. Share prices can, at times, rise hard and fall fast. But the long-term trend is very steady. There is only one 10-year period in US history that has given negative returns – and that was due to the great crash of 1929. Out of more than a hundred rolling

10-year periods, only four produced no growth (ie, a return close to zero). At least 95% of the time, therefore, any

10-year holding period was going to give you a positive result. Looking at the JSE since 1960 (rolling 10-year periods starting every month end), there is not a single negative return. Assuming the re-investment of dividends, there is in fact only one

10-year period (out of over 500 ten-year spans) which produced less than an 80% return. Over the half century since 1960, there was a 97.6% chance of at least doubling your money over any 10-year

period (ie, starting any month since January 1960). More impressively, the average 10-year

return over 509 periods, with dividends re-invested, is almost 500%.

In short, the risk of actually losing money in the stock market, over the longer term, is very very low. The risk becomes almost zero if you apply two simple principles: (1) don't buy when the market is over-heated, and (2) apply rand-cost averaging (ie, keep accumulating shares at different price levels, especially when the market is falling).

For the long-term investor in shares, the risk of capital loss is very low and the chances of making a good return are relatively high – especially if you are able to skew your portfolio towards above-average shares. Provided you have a long-term perspective, therefore, the stock market is not the high-risk environment it is often thought to be.

The ShareMagic™

advantage

The facts and figures above amply demonstrate the high gain, low risk position of the typical long-term stock market investor. All of these figures use stock market indices, which show the average performance of the share market. As a private investor – as we explain in another article – you have the advantage of being able to do a little better than the market average, giving you the potential of outstanding returns.

With its intuitive interface and full integration, ShareMagic™ gives you the information you need to find those above-average shares quickly and easily. Put yourself in a position to capitalise on the investment power of the stock market – pick up the phone today and speak to one of our friendly consultants.

Call +27 11 728-5510 now to get started

PS To find out more about ShareMagic™ solution,

click here to get an overview of the complete product range. Or phone +27 11 728-5510 now to arrange a no-obligation demonstration.

PPS For the record, the risk of losing your money due to fraud in the share market is almost nil. In South Africa, JSE stockbrokers are very strictly regulated and the JSE runs a guarantee fund to protect investors in the event of default. Provided you use a reputable broking firm, money you invest in the JSE is as safe as houses (pun intended).

|